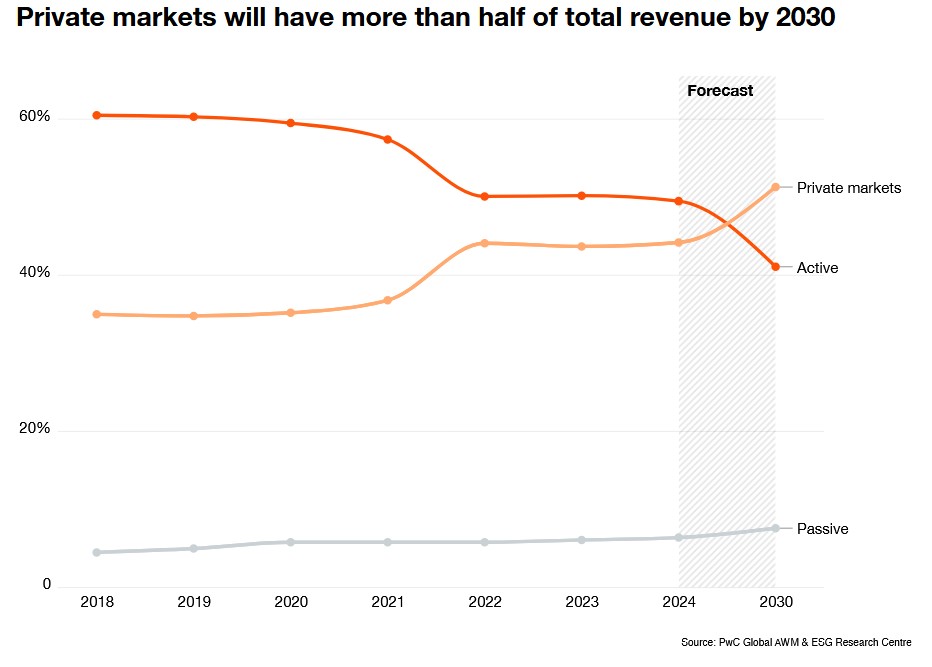

Private market revenues are set to reach $432.2 billion, accounting for more than half of the total global asset management industry’s revenues by 2030, a report from PwC released today finds.

PwC’s 2025 Global Asset & Wealth Management Report, based on a survey of 300 asset managers, institutional investors and distributors from 19 countries and 10 territories, also said that global assets under management are projected to rise to $200 trillion by the end of the decade. It stood at $139 trillion in 2024. That equates to a compound annual growth rate of 6.2 per cent; total investible wealth worldwide is expected to exceed $481 trillion, the report said.

The expansion of private market investing has been a dominant wealth management theme in recent years, fueled by more than 10 years of ultra-low interest rates after the 2008 financial crisis, a structural shift from listed equities, and a desire for more diversification. A rising use of “passive” investment entities such as exchange-traded funds has squeezed asset managers’ fees, while private market investment fees tend to be higher – understandably encouraging fund distributors to sell them to clients such as wealth managers, family offices and private banks.

PwC said private markets are set to “remain the industry’s most profitable engine.”

Private markets generate roughly four times more profit per billion dollars of AuM than traditional managers today. By 2030, private markets revenues are set to reach $432.2 billion and deliver over half of the total asset management industry’s revenues by 2030.

The squeeze

In general, however, profitability pressures and narrowing margins amid tough competition, fee pressure, a premium on talent and expensive investments to increasingly diverse and sophisticated client origins create challenges, the 20-page report said.

A large majority – 89 per cent – of asset managers reported profitability pressure over the past five years – with PwC analysis finding that profit per AuM has declined by 19 per cent since 2018, with a further market-wide 9 per cent decline expected by 2030.

Costs remain the most visible driver of the squeeze – with more than two-thirds of every dollar consumed by such costs, the report said. Almost three-fifths of institutional investors say they are likely or very likely to replace managers purely due to high fees.

The report helps illuminate why there has been considerable wealth management industry M&A in parts of the world. In the US registered investment advisor sector, to take just one case, there were 273 transactions completed in 2025 as of October 28, DeVoe & Company said a few days ago, confirming that this year has already beaten the full-year record of 272 transactions.

Convergence

The PwC report said that in such a challenging environment, asset managers are “targeting convergence” with wealth managers and fintech firms to build “technology-enabled ecosystems”; they see integrating AI and automation as the most significant way of making their businesses more resilient by 2030.

“Asset managers are evolving in the Intelligence Age, as new technologies – from generative AI to agentic AI – re-shape how value is created and delivered. The winners won’t be those who gather the most assets, but those who rewire fastest, translating innovation into digital ecosystems that serve more diverse investors, more personally and efficiently than ever before,” Albertha Charles, global asset and wealth management leader, PwC UK, said.

North American dominance

In estimating the likely growth of AuM, the study said North America will remain the dominant market, rising rise at a CAGR of 6.2 per cent. However, Asia-Pacific is projected to grow fastest at a CAGR of 6.8 per cent. Latin America , the Middle East and Africa and Europe are also expanding, it said.

The total pool of global investible wealth is set to climb from $345 trillion in 2024 to $482 trillion by the end of the decade – a CAGR of 5.7 per cent.

Two-thirds of this growth will be driven by structural and demographic shifts among mass-affluent individuals and high net worth individuals.

Tokenization

PwC said that besides the revenue allure of private markets, another bright spot includes tokenized funds. AuM is projected to grow at a staggering 41 per cent CAGR, from about $90 billion in 2024 to $715 billion by 2030, driven by the maturation of blockchain infrastructure, institutional adoption, as well as the democratization of private markets.

Elsewhere, passive AuM is projected to rise at a CAGR of 10 per cent, to reach $70 trillion by 2030.

Archetypes of success

Businesses best positioned to outpace and outcompete are clustering around four distinct models – yet only 42 per cent of firms today fit one of four winning archetypes, PwC said.

The four models are “full scale private-to-public hypermarkets ; solutions platforms ; low-cost manufacturers ; and niche champions .

The report said that other models outside the four main categories will only be able to capture 6.1 per cent.